Kiska Metals: a nickel still goes a long way!

Nov 22

Kiska Metals (CVE: KSK) (OTCMKTS: KSKTF) is in the business of “prospect generation”.

Exploring for precious commodities like gold and copper is a risky business. When you’re right, it’s like winning the lottery. You become a millionaire or billionaire overnight. But when you’re wrong, as 95% or more of exploration companies drilling grassroots projects will be, the losses can be devastating. As in lose your entire investment devastating.

The happy medium

On paper, the prospect generator model eliminates the odds of owning 100% of nothing.

According to the law of averages, assuming Kiska stays in the game, it must win eventually—and in this game one BIG win can more than compensate for dozens of losses.

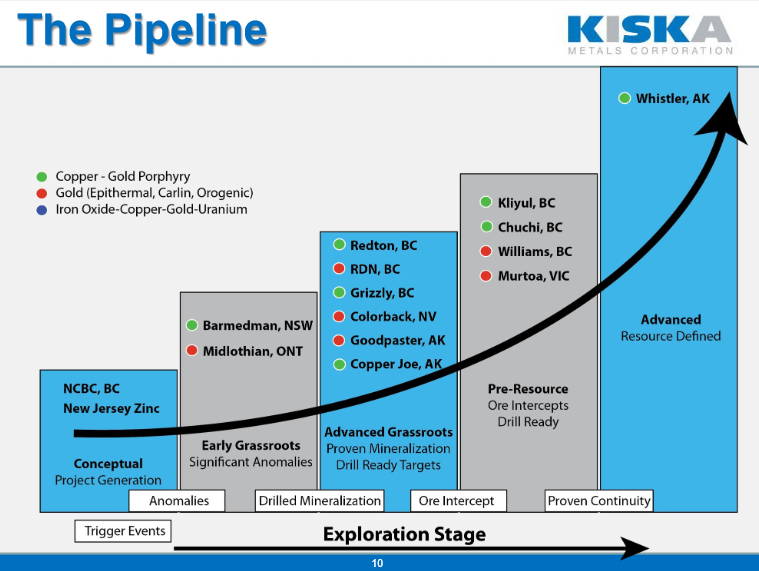

Outfits like Kiska Metals hedge themselves and limit risk by securing (staking and claiming) prospective land packages, then using other people’s money to prove or disprove Kiska’s geological interpretation(s) via drilling. The image below represents Kiska’s pipeline; which one of these properties will provide the big win investors are hopeful for?

Why would other people risk their money to advance Kiska’s projects?

Currency (Eg. paper money) is readily available. For some, it can be created with the push of a button… like magic. For others, it can be borrowed at interest rates so low it’s practically free. Therefore, it’s the lands, minerals, and skilled people that are in short supply—those are the scarce resources.

Why would other people risk money on Kiska’s projects? Simply put, Kiska has a knowledgeable and capable team of geologists that specialize in grassroots exploration. Those with access to capital whom are not in the business of making mineral discoveries want to partner with Kiska. At the end of the day, they fund a vast majority of Kiska’s exploration and drilling in exchange for an ownership stake in the underlying property / project.

In a perfect world, these partners are mining companies with engineering expertise and financial muscle. Ultimately, they write a fat check to buy the property outright or agree to fund it through production, leaving Kiska (or prospect generators like them) with an ownership stake or royalty. Through this process Kiska strengthens its balance sheet and finds more time to focus on what it does best, generate prospects… The End.

When buying Kiska what do you get for your nickel?

At recent market prices of $0.05 Kiska’s entire business is valued at $6.4 million.

Tangible and intangible assets include:

a) Geographically diverse portfolio of 14 distinct projects — Alaska, BC, Nevada, Ontario, Yukon, Australia

b) Royalty portfolio covering 12 properties — 0.5% to 2% NSR

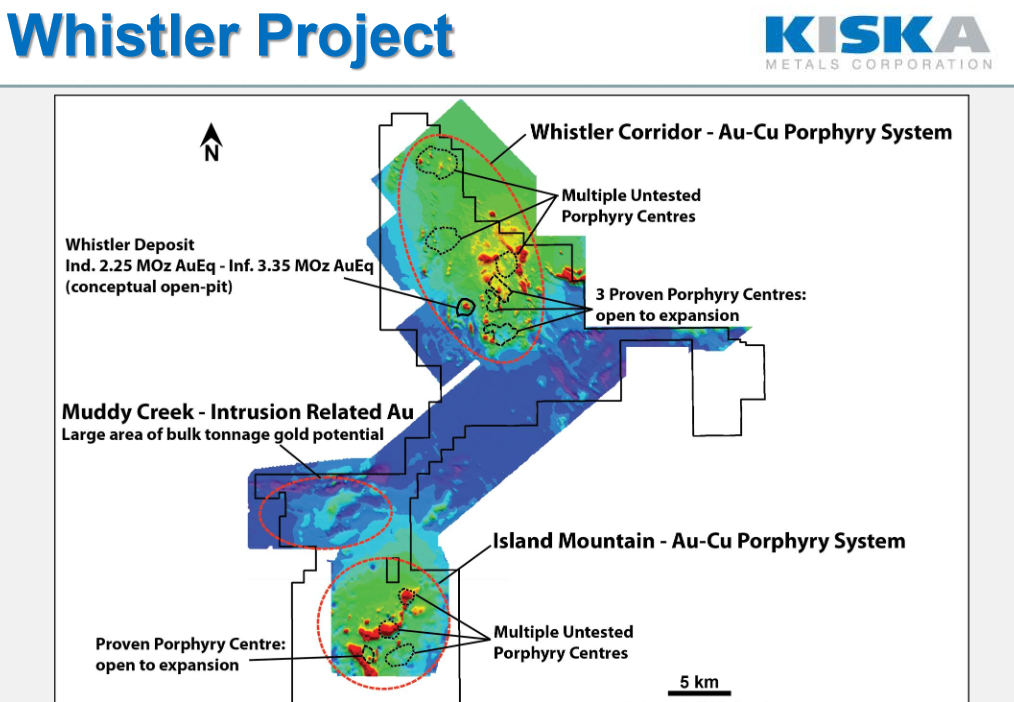

c) Gold equivalent resource of 5.6 million ounces in the indicated (40% in the indicated category) and inferred categories at Kiska’s 100% owned, district scale (100,480 acres) Whistler Project

d) Extensive New Jersey Zinc database — spans nearly 150 years’ worth of base and precious metals exploration activity worldwide

e) “Top-Drawer” technical expertise, including geologists that were winners of the world famous *Goldcorp Challenge. Prospect generation is in Kiska’s genes, it formed from the merger of Rimfire Minerals and Geoinformatics Exploration back in 2009.

Going through the big D (and don’t mean Dallas)

Admittedly, the entire metals and mining industry is depressed, with a capital D.

Despite the fact that many of Kiska’s potential partners have been sitting on their hands (waiting it out), its current roster of JV partners includes respected names such as Newmont, Teck, and First Quantum.

Kiska has roughly $1.3M cash at the moment. With any luck, that amount could buy them another year, which could be all it takes for a breakthrough at one of the projects or the market to turn (fingers crossed… avoiding a dilutive nickel-priced financing). A somewhat unexpected near term cash injection might come from a 0.5% net smelter return (NSR) royalty Kiska owns on St. Andrew Goldfields Holloway Mine. Kiska is currently in friendly negotiations with St. Andrews regarding $999,315 or so of missed payments. This particular royalty includes 10 kilometers of strike length along the Porcupine – Destor fault, a gold rich region, so the NSRs life should be long.

Additionally, it’s important to know that Kiska has a few committed shareholders like Sprott (5% owner) and Geologic Resource Partners (25%) that could act as financial backstops in a worst case scenario.

What might we expect from Kiska in 2015?

Mentioned above, Whistler is Kiska’s most advanced project. Once upon a time major mining outfits were attracted to large copper-gold porphyry deposits such as Whistler, but items like development cost and accessibility have trumped size and potential in the minds of decision makers lately.

However, psychology changes, and proposed initiatives like Alaska’s Road to Resources could go a long way toward improving Whistler’s accessibility in the coming years. Kiska’s search process for the right partner at Whistler is ongoing. Any news that moves the project forward should have a positive impact on the share price.

Kiska’s “Looking Ahead” slide in its investor presentation says to expect news flow related to Teck’s work at Kliyul. Teck can earn a 51% interest in the Property by incurring a cumulative aggregate of $5.5 million in exploration expenditures on the Property on or before January 31, 2018. Furthermore, between now and March 31, 2015 First Quantum will be finalizing (or not, but either way Kiska will know something) its agreement with Kiska on the Copper Joe Project. As per the Letter Agreement, First Quantum can earn an initial 51% interest by funding expenditures of $5M by December 31, 2017.

Also, look for Kiska to settle its dispute with St. Andrew Goldfields, this could provide a lump sum payment of up to $1M and a solid revenue stream moving forward.

Bottom Line: Kiska is a legitimate penny stock speculation (the only type PennyStockExperts.com aims to present) for anyone interested in gaining exposure to precious and base metals. Compared to many of its peers, Kiska offers a lot of bang for the buck— or nickel in this case.

Based off the three metrics below, Kiska looks interesting:

1) With a market value of $6.4M new shareholders are paying roughly $2.13 for each ounce of gold believed to be in the ground at Whistler, the +700 million pound copper resource would be free. Obviously, this metal may never see the light of day, but it’s not going to walk away either.

2) Assuming all properties are equal (just play along here…) a new shareholder is paying $457,142 Canadian dollars for each of Kiska’s projects. Of course, that would assign zero value to any of the 12 royalties in its portfolio. Not including the Nevada properties, Kiska controls 440,618 acres worth of claims in total.

3) Technically speaking, Kiska shares bottomed during November 2013 (at least for now) at $0.04. From there it bounced 300% off what could prove to be the all-time low. Today’s prices represent a good risk/reward, as shares of Kiska Metals try to find support around the four to six cent levels.

Bookmark PennyStockExperts.com, subscribe (with just an email) to receive our truly independent reports in your mailbox, and look forward to a deeper dig into Kiska Metals with its CEO Grant Ewing, P.Geo. Audio interview coming soon!

*Some geologists that were associated with the team who won the Goldcorp Challenge are no longer employed by Kiska Metals