2 Respectable Gold Exploration Stocks Trading Below NAV

Apr 29

Nearly every stock associated with precious metals has increased dramatically in the past six months (we’re talking 50% to 500%).

While not all deserved the price appreciation, it happened anyway.

As a consequence, not many “super bargains” remain. A few months ago high-quality miners could be scooped for less than five-times operating cash flow. Explorers with quality resources could be had for less than cash on hand.

–now the cost is much higher. In a way, it’s kind of sad, isn’t it?

Consider the crowd psychology/thinking over recent history:

a) Gold stocks down relentlessly! Losing money = financial pain (mental anguish even migrates into the physical realm for some). Who mustered up the courage to “buy low” aggressively? i dunno, perhaps 5% of all participants?

b) Now then, inventory levels of “the right products” are way too low (aren’t they always approaching bear market finales). This leads to more mental anguish; 95% of the crowd is under-invested. Or worse yet, they sold too early. Shit! Damn!!… Must. Have. Pullback. has become the mantra for many since January.

HUI Gold Bugs Index — 5 Years Down vs 4 months Up

Let’s face it, for one’s gold stocks portfolio, capturing 25-50% (or hell, even 100%) doesn’t feel like “winning” after watching the old brokerage account hemorrhage year after year after year. The feel-bad-factor is compounded upon watching previously held gold stocks continue to race higher, almost daily.

If you’re still waiting for that pullback… i admire your patience.

In the 2014-2015 time frame, after years, months, and occasionally hour-to-hour bouts of mental turmoil even the most stubborn gold bulls threw their hands up and towel in (a good buy signal in my experience).

Damn it! This shit ain’t easy!! It never is.

Personally, this is when i’d try to comfort myself with a reminder, even The Gurus and TV Investment Celebrities get it wrong once in a while, or even most of the time (that feels better, ahhh).

Dan (i’d say to myself), if you wanted to be right 10-of-10 times you should have been an engineer. With stocks, “being right” 100% of the time doesn’t exist. Selling at the top and buying at the bottom, while carrying the perfect level of inventory– i’m afraid it only happens once or twice in a lifetime, if you’re lucky.

That’s just the reality.

Getting to the point here (please forgive me if i rambled), the moral of the story is that more and more speculators/investors are jumping on the “gold bull market bandwagon” each week.

Indeed, very few super-duper bargain stocks remain today, as compared to December 2015.

However! I’ve done the digging and back breaking number crunching on your behalf. Below you will discover two gold exploration stocks priced below, or precisely near NAV (with a brief description of each). Far as i can tell, each is led by proven prospectors/geologists/dealmakers whom have made discoveries, and have skin in the game.

–i’ve been told that’s what a stock market prospector should be looking for

2 Respectable Gold Exploration Stocks (still) Trading Below NAV

1) Benton Resources (CVE: BEX) (OTCMKTS: BNTRF)

Led by the Stares Brothers, Stephen and Michael, Benton Resources has a relatively young and aggressive team. Worth noting, in 2007 the Stares Family received the Bill Dennis Prospector of the Year Award. This award was given by the Prospectors and Developers Association (PDAC) to recognize the family’s contributions to the industry over the past 40 years.

Via Benton Resources, a proud family tradition lives on.

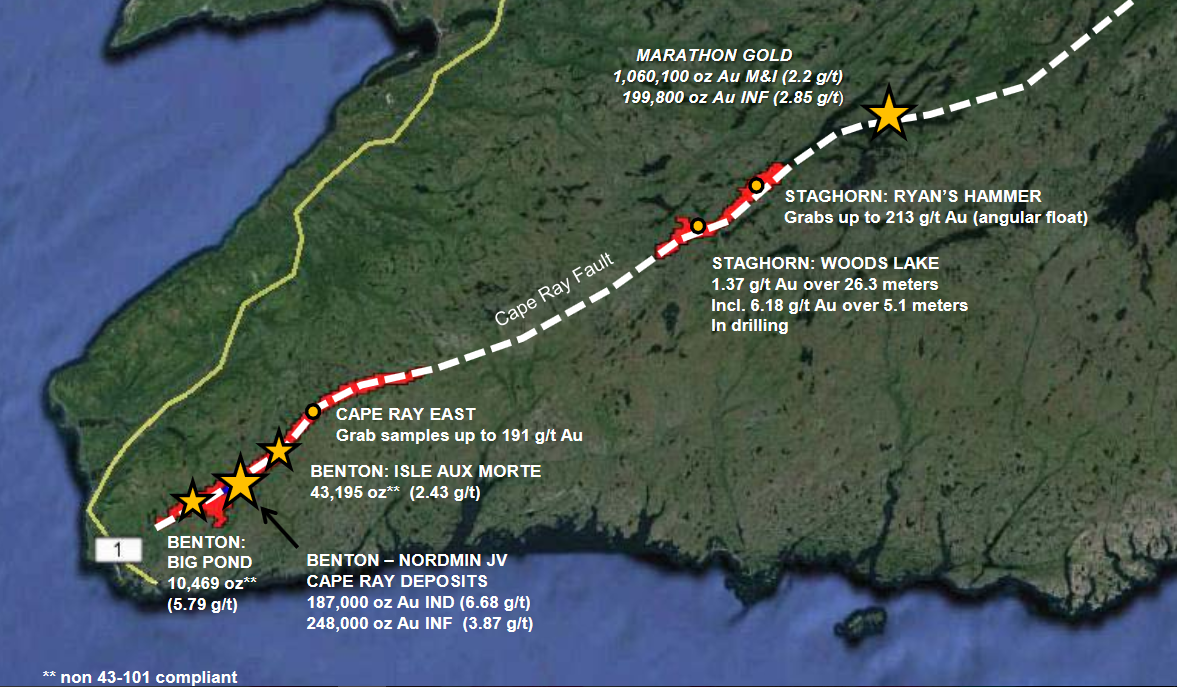

At any given time, Benton Resources is staking, testing, and hopefully upgrading a roster of 5-10 projects. Presently, “Cape Ray” is its flagship project. Located in mining-friendly SW Newfoundland, BEX controls (after years of consolidating) a strong land package straddling the Cap Ray fault.

Benton’s Land Position in Red

Just to the north, Marathon Gold (TSE: MOZ) has delineated a +1 million ounce resource it calls Valentine Lake (also on the Cape Ray fault).

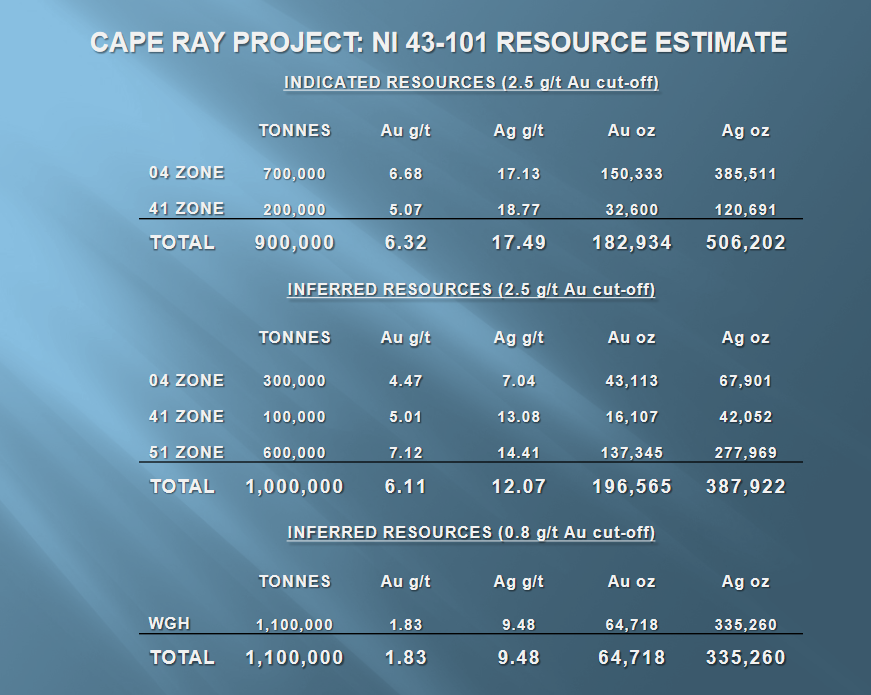

Thus far, Benton Resources has delineated around 400k ounces of indicated and inferred among three zones. Pretty good grades, and some phenomenal, have been intercepted at or near surface. The existing resource averages +- 6.2 g/t Au and 14.5 g/t Ag (using a 2.5 g/t Au cut-off), it remains open in most directions and at depth.

Benton’s Cape Ray Resource Estimate — From Investor Presentation

Also interesting, Nordmin Engineering is fully-funding the advancement of Cape Ray until a production decision is made. As it stands, the PEA shows a post-tax IRR of 24% (at $1200 gold) and pre-production costs of $47.3M for an 850tpd mill. In the near future, Benton Resources and 80/20 partner Nordmin may move forward with a 10,000-20,000m drill program and feasibility studies (funded by Nordmin). With only 15-20% of Cape Ray thoroughly explored, the odds are reasonable it, like Valentine Lake to the north, will grow to the million-ounce mark.

*BEX Market Valuation at 4/29/16 = $3.85M [approx. $4.3M cash and marketable securities]

**Insiders, friends and family of Benton Resources own +10% equity and have been buying in the open market recently

2) Golden Valley Mines Ltd. (CVE: GZZ) (OTCMKTS: GLVMF)

Led by CEO Glenn J. Mullan, Golden Valley Mines has a long history of being in the right place at the right time. Therefore, i’m pleasantly surprised we can buy everything Glenn’s Team has put together (+80 grassroots projects in the famed Abitibi) for $0.

How do i arrive at the zero valuation?

Follow me>>> looking underneath the hood we notice Golden Valley Mines owns 51% of Abitibi Royalties Inc. (CVE: RZZ), of which Mr. Market, in all his pricing wisdom, assigns a value of $47M. While GZZ doesn’t plan to sell this core holding, it’s worth $23M on paper (more than its market cap).

To be fair and balanced, let’s assume Abitibi Royalites goes down, won’t GZZ go down too?

–most likely, so consider it a gift when it happens

Abitibi Royalties’ currently owns about $39M worth of Agnico Eagle (NYSE: AEM) and Yamana Gold (NYSE: AUY) shares. This implies its numerous Canadian Malartic royalties, offering exposure to all stages of mining at Canada’s largest producing gold mine are worth $8M. Considering it expects to generate cash flow of $2-$2.5M in 2016 (roughly 18-23 cents per share), perhaps adding more in 2017 when Jeffrey and Barnat move into production, the Malartic royalty interests are an intriguing buy at today’s price (GZZ is how i’m playing it).

–to summarize, $8M seems a reasonable price to pay for $2M cash flow

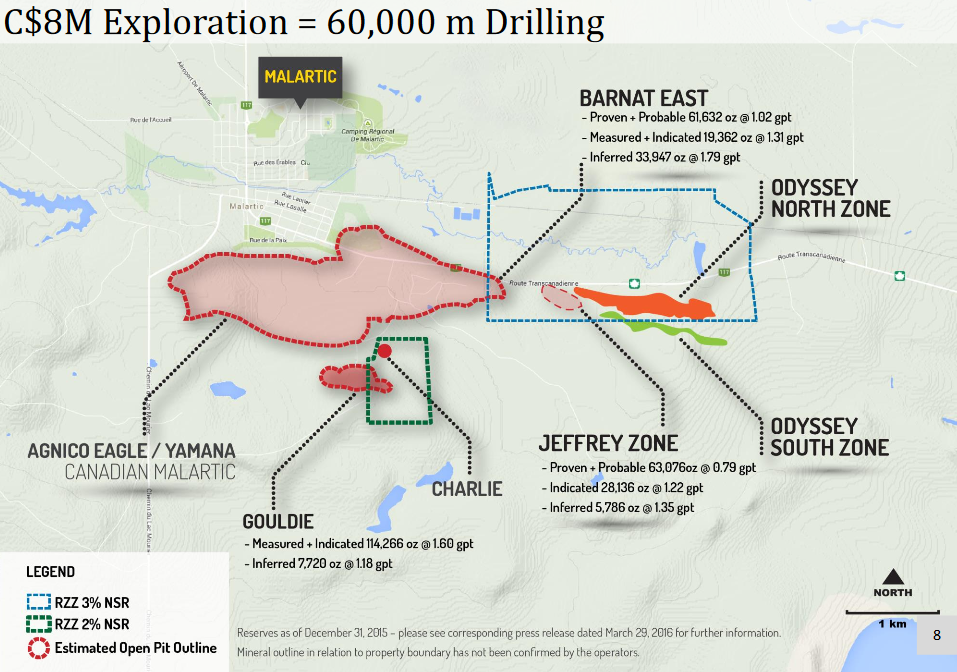

But there’s more! The crown jewel in Abitibi’s royalty portfolio may be its “Odyssey North” 3% NSR; we hadn’t factored that into the equation yet! This year Agnico/Yamana plans to drill 60,000m at Odyssey North, upping its original estimate after intersecting holes like 2.12 g/t Au @ 70m and 2.85 g/t Au @ 110m.

NSR Map — Abitibi Royalty Holdings in Canada’s Largest Gold Mine

Getting back to “the people factor”, i mentioned Golden Valley Mines has a history of being in the right place at the right time. Glenn J. Mullan staked the Malartic CHL Project in 2006 (now Abitibi Royalties’ key asset) as part of an Abitibi Greenstone Belt exploration program which tested 195 targets on 52 properties to date.

More recently, speculators seem to be excited about Sirios Resources (CVE: SOI) and its Cheechoo discovery in the James Bay region of Quebec. Golden Valley Mines optioned this property to Sirios. GZZ utilizes a “prospect generator” business model which aims to minimize downside (by farming out risk) and maximize upside (by holding royalties or partnering projects). Upon completing its earn-in, Sirios owes Golden Valley $500k, a 4% royalty on Cheechoo, and shares, of which GZZ owns about three million.

Is it just me, or does Golden Valley Mines seem to have a habit of being in the right places?

From my research and speaking with Glenn J. Mullan briefly, i believe he’s a guy worth betting on (and the cost of doing so is nearly $0 right now), if past is prologue he will continue winning.

*GZZ Market Valuation at 4/29/16 = $22.4M [approx. $25M cash and marketable securities]

**CEO Glenn J. Mullan is the 2nd largest shareholder

*Author has a long position in Benton Resources and Golden Valley Mines Ltd.

DISCLAIMER: The information in this publication is not intended to be, nor shall constitute, an offer to sell or solicit any offer to buy any security. The information presented on this website is subject to change without notice, and neither Penny Stock Experts nor its affiliates assume any responsibility to update this information. Additionally, it is not intended to be a complete description of the securities, markets, or developments referred to in the material. Penny Stock Experts and its Author(s) cannot and do not assess, verify or guarantee the adequacy, accuracy or completeness of any information, the suitability or profitability of any particular investment, or the potential value of any investment or informational source. Additionally, Penny Stock Experts and its Author(s) in no way warrants the solvency, financial condition, or investment advisability of any of the securities mentioned. Furthermore, Penny Stock Experts and its Author(s) accept no liability whatsoever for any direct or consequential loss arising from any use of our product, website, or other content. The reader bears responsibility for his/her own investment research and decisions and should seek the advice of a qualified investment advisor and investigate and fully understand any and all risks before investing. Information and statistical data contained in this website were obtained or derived from sources believed to be reliable. However, Penny Stock Experts and its Author(s) do not represent that any such information, opinion or statistical data is accurate or complete and should not be relied upon as such. This publication may provide addresses of, or contain hyperlinks to, Internet websites, Penny Stock Experts takes no responsibility for the contents thereof. Each such address or hyperlink is provided solely for the convenience and information of this website’s users, and the content of linked third-party websites is not in any way incorporated into this website. Those who choose to access such third-party websites or follow such hyperlinks do so at their own risk. The publisher, owner, writer or their affiliates may own securities of companies mentioned in this publication.